In my last post, When Various Monetary and Market Forces Converge, we looked at Basel III. As you can see from the description below, these changes have a major impact on risk management and the QUALITY of capital banks are holding. While these rules go into force on July 1st, arriving at the “third of the three Basel Accords” has taken a while.

[Basel, Switzerland has been the home of The Bank of International Settlements, the central bankers bank, and arbiter of global banking regulations.]

The next B we must look at, happens just days after the Basel III, an annual BRICS meeting that takes place in Rio de Janeiro on July 6-7. Let’s dive in.

Aircraft Carriers, Not Speedboats

When we think of “the market”, most people think of stocks. When we think of money, most Americans think of cash. Cash is classified as “risk free”. Stocks are “risky”. Yet, the value of a currency is always changing in international banking and trading, just like stocks.

To gain a better understanding of where world finance arrives as the BRICS nations meet in July, we must examine changes that have occurred at the aircraft level over years, not days.

While there are many brilliant individuals watching and speaking about this BRICS meeting and their objective of reducing the dollar’s dominance in world trade, my comments have been influenced heavily from writings of James Rickards recently, and his book mentioned in the last post, The Death of Money (2014).

Their main objective has been to gain power on global governance. This includes a pursuit of expanding the UN Security Council to include Brazil and India. The council would have to approve this increase to 7 seats, which if approved would give the BRICS nations 4 seats, a majority. (pg 147, The Death of Money, 2014)

We welcome the discussion about the role of the SDR in the existing international monetary system including the composition of the SDR’s basket of currencies. (pg 149, ibid)

Rickards boils this down to one theme: “the diminution in the dollar’s international role and a decline in the ability of the United States and its closest allies to affect major forums and in geopolitical disputes. (pg 150, ibid)

What are NOT BRICS objectives for this Summit

The BRICS nations do not have a free-trading area like the European Union except on a bilateral basis. (pg 147, ibid)

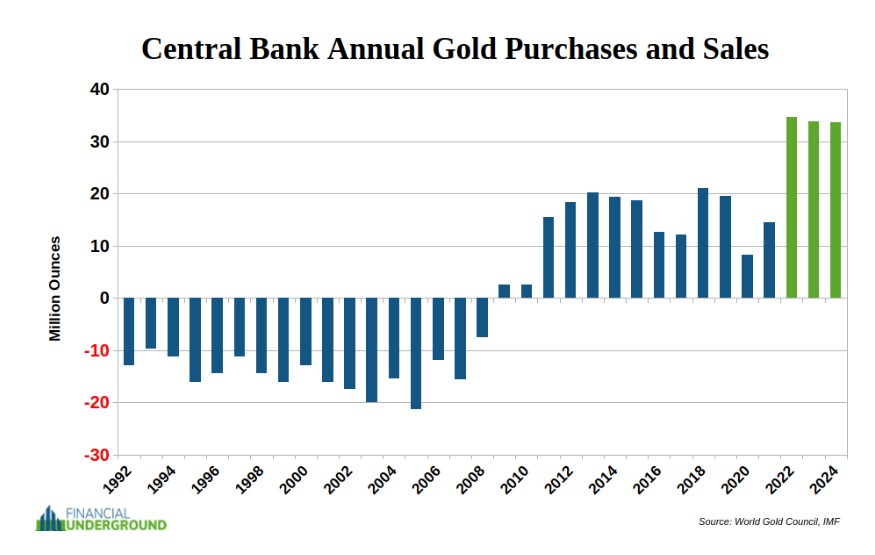

Russia – gold reserves have increased from 531 metric tonnes (mt) to 2,333 mt.

China – increased gold reserves from 600 mt to 2,293 mt

Indian – increased gold reserves from 358 mt to 880 mt

Conclusion

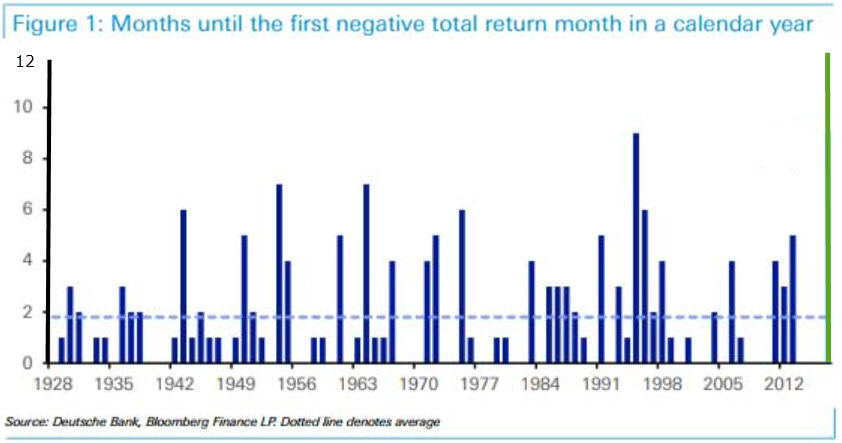

The biggest problem with the financial picture we are all watching today, is that these 4 major countries – Germany, France, Japan, and the United States – have seen their major stock indices reach their highest levels ever in June 2025, or have stalled in the last 15 months. This does not mean they will not continue to climb over the short term. However, when we consider that we are now 16 years since the 2009 low, AND we have yet to see a decline in the S&P 500 last more than 7 WEEK period, RISK planning must be on every investors mind.

Will the stricter capital requirements by the Basel III requirements and the actions of BRICS nations in the second half of 2025 have a major impact on global financial markets?

My next post will be the last B, bonds. We will return to trends I have talked about since 2020. They are like gravity, a force that is above the power of mortals to control.

Who has directed the Spirit of the LORD, or as His counselor has informed Him?

With whom did He consult and who gave Him understanding? And who taught Him in the path of justice and taught Him knowledge and informed Him of the way of understanding?

Behold, the nations are like a drop from a bucket and are regarded as a speck of dust on the scales; Behold, He lifts up the islands like fine dust.

Over the last several months I have been collecting articles as well as watching market patterns from a variety of experts. Some are newer to me than others, but all have a long history. Because I see these trends converging as we go into the 3rd quarter this year, I feel compelled to share this collection of patterns with you now. For me, these are so large that collectively, they could have a global, if not historical, impact.

Since you are reading this, I doubt this sounds like hyperbole from what we have watched since 2020. Some trends span not only years, but decades. If we had time, we could unfold trends going back centuries, or millenniums if we wanted to learn from antiquity, but we must move on.

The “Golden” Rule Change at the Top of Central Banking

On July 1, 2025, the Bank of International Settlements, the global hub of all central banking, are set to make changes in what is known as Basel III, a set of capital requirements on banks globally. According to Scottsdalemint.com, these are certainly needed:

The much needed change strengthens bank capital requirements, limits leverage, and increases liquidity standards to reduce financial risk and enhance banking system stability.

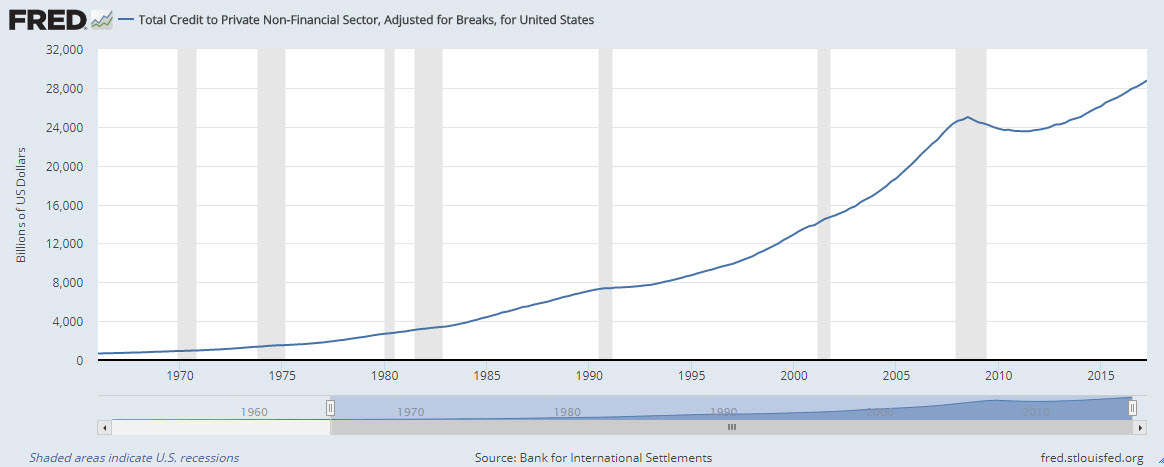

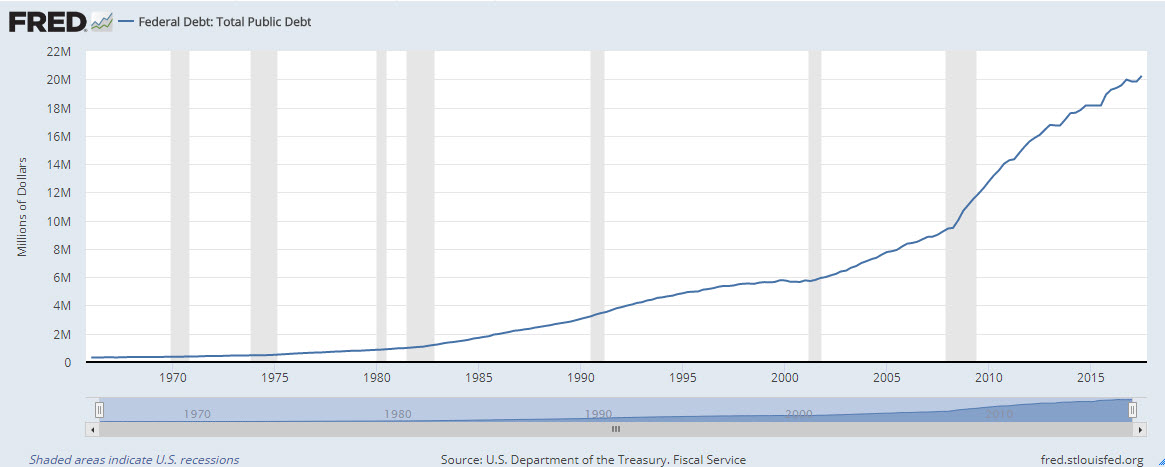

Wow, and the world’s highest banking officials could not figure out that all the DEBT THEY financed and fueled between 2008 (Global Debt $173 trillion) and the end of 2024 ($318 trillion) might just create too much leverage and instability?

Previously, banks could hold gold on their balance sheets in the form of unallocated paper gold contracts without holding physical gold in tangible form. These paper contracts were considered as “good as gold” when it came to determining how much capital a bank needed to maintain on its balance sheet. Under the old rules, there was little incentive to hold physical gold, as it was only valued at 50% for reserve purposes. Basel III rules move physical gold from being considered a Tier-3 asset to being considered Tier-1, which allows physical gold in bullion form to be counted at 100% value for reserve purposes. Gold in unallocated paper contracts will no longer be considered an equal asset. For this reason, banks using paper forms of gold to help meet reserve requirements will have to convert those positions to physical metal, or risk becoming too undercapitalized to continue to function. [Bold and italic text mine]

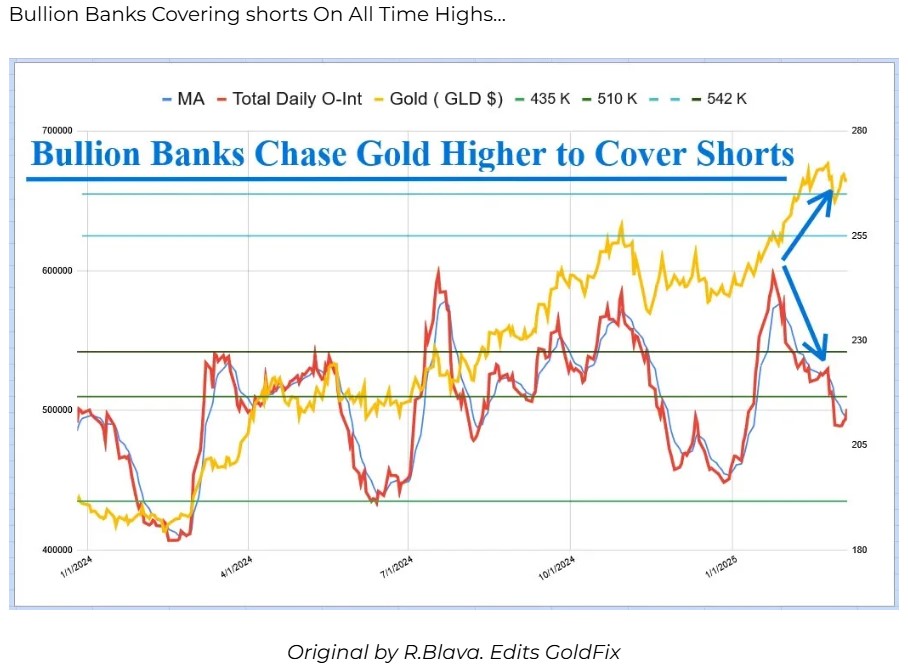

While you may have come to believe early this spring that the gold flown into New York banks from the London Bullion Banks was from fear of future tariffs, the coming of Basel III regulations moving gold to a Tier 1 asset, combined with gold prices climbing sharply since 2023, FORCED them to eventually close out short positions in the gold FUTURES markets, thus having an immediate impact on them.

Last year, central banks purchased approximately 34 million ounces of gold, marking the third consecutive year of near-record buying….

Central banks and governments are the largest single holders of gold in the world. Together, they officially own over 1.2 billion troy ounces—out of the 6.9 billion ounces humans have mined throughout history.

Russia and China—the US’s top geopolitical rivals—have been the biggest gold buyers over the last two decades.

As we come through June 2025 and head into the 3rd quarter, I think about these words written in James Rickards 2014 book, The Death of Money: The Coming Collapse of the International Monetary System.

“Most profoundly, a new gold standard would address the three most important economic problems in the world today: the dollar’s decline, the debt overhang, and the scramble for gold.” [page 241]

Think about those 3 things: debt overhang, dollar decline, and scramble for gold. That was 11 years ago. Are these huge issues not even more impactful on our world in 2025?

In Part 2 of this 3-part series, we will look at the debt overhang and the BRICS as we move toward a term we must understand, a multipolar monetary system. The BRICS meeting in Rio de Janeiro, Brazil on July 6 and 7 may be as important to watch as the reaction to the implementation of Basel III bank changes that goes in effect on July 1st.

I know these are huge trends and issues we cannot control. However, they are influencing the world we live in and our lives. We must investigate them. We must seek to understand how they could impact us.

Back soon.

“Nothing in all creation is hidden from God’s sight. Everything is uncovered and laid bare before the eyes of Him to whom we must give account.” – Hebrews 4:13

In my last post, “WHOse Life is it Anyway?”, we looked at evidence that showed that powerful globalists groups met in New York in October 2019. The gathering was called Event 201. The event included the John Hopkins Center of Health Security, the World Economic Forum, and the Bill and Melinda Gates Foundation.

The entire world knows what happened as we rolled into 2020. It is part of our collective history.

But how many individuals in 2024 know about Event 201? Why was this event not a major news story at the time? How many have had a chance to consider WHY these globalists groups ran through a “high-level pandemic exercise” shortly before we began to hear that a virus had leaked from a lab in China? How many today remember that SARS-CoV-1 came out of China in the spring of 2003, giving the world’s health “experts” many papers published in major medical journals for almost 2 decades before SARS-CoV-2 hit the world?

What happened to drive the world into its first ever lockdown, yet without world health authorities discussing treatments that proved successful in treating SARS-CoV-1 years before?

One thing that has become clear since my first public article in 2005, is that we are living our lives like a game. Take any subject and create conflict between the two groups. These could be labeled group A and B. Group C would be in the planning position to influence the narrative in a direction, thus keeping Group A and B moving in a direction always labeling comments that bring negative attention to their plans as a “conspiracy theory” or “disinformation”.

The Players in The Game

Neither A nor B would want to fully follow Group C, so misdirection had to be a common theme of the actions of Group C. This is not to say that there have not been conspiracy theories that proved to be false, but that this tool has been used for generations by Group C. An understanding of Hegel’s Dialectic is a major tactic that has impacted the world to bring us to where we are at this point in history, a tool widely used by Group C.

The great tragedy of Communism, however, is the fact that its founders did not stop at the so-called “harmless speculation” of Dialectical Materialism. They determined to permeate every aspect of human existence with the principles which they felt they had discovered. Therefore, they promoted a new approach to history, economics, politics, ethics, social planning and even science. In the Communist Manifesto (first publ. in 1848), Marx and Engels admitted that critics of Communism could say that it “abolishes eternal truths, it abolishes all religion, and all morality, instead of constituting them on a new basis; it therefore acts in contradiction to all past historical experience.” [The Naked Communist, first published in 1958, 2014 edition, W. Cleon Skousen, pg 40]

Group D is a group that tries to stand outside the game, considering the actions of Group C (continuing to misdirect, YET, with a purpose), however finding it difficult to discuss with a larger group because of an understanding that the entire crowd is being lead in a negative direction.

Since COVID in 2020, I believe the size of individuals in Group D has exploded worldwide and continues to grow because of the actions of those in Group C.

Planned Fear, Planned Pandemic

We know that Event 201 took place with various globalist actors conducting a simulated pandemic before the world went into lockdown from COVID – 19.

If some of the same globalists’ actors conducted another simulated pandemic, see also Catastrophic Contagion, in October 2022, would we really be surprised to see another planned pandemic?

What about the current headlines on monkeypox and the avian bird flu?

Headlines: Narrative Media Promotes Fear / problem / Group C

Taking the same two articles, and like COVID 19, we find the media, globalist solution continues to be.…. vaccines are ready.

The CDC recommended last week that people in the US who are exposed to or at high risk of catching mpox should get vaccinated….

Half a million doses of the vaccine are in stock, and another 2.4 million could possibly be produced by the end of the year, according to Tim Nguyen of the WHO Health Emergencies Program. The DRC and Nigeria will be the first to receive these vaccines, African Regional Emergency Director Dr. Abdou Salam Gueye added. (CNN/1)

A quiet effort to prevent the next global pandemic began rolling off an assembly line this summer behind the gates of an office complex in suburban Raleigh.

In this sprawling factory, sheltered by thick pine groves, workers at CSL Seqirus are bottling millions of doses of a new vaccine targeting the H5N1 bird flu virus. (USA Today/ 2)

Independent Medical Commentary/ Group D

If there ever was a time to learn to think for yourself and NOT follow the mainstream media narrative, it is now. The following are comments about these two viruses, and vaccines already being produced as the solution to the viruses. Like 2020, the narrative is not discussing safer drugs that were used worldwide successfully for decades before…and since 2020.

I would strongly encourage you to subscribe to Dr. McCullough’s substack. Since COVID 19 came on the world scene, he has been one of the top authorities in the world fighting relentlessly to bring truth to the constant stream of disinformation presented by globalists organizations.

The following are just a few points I learned from an interview by John Leake in a post called, How to Avoid Another Campaign of Fear – Disease X Bird Flu, July 19, 2024

Bird flu has been around for over 100 years. Throughout history, about 800-900 cases have brought about death. The main spot in the world where these deaths have occurred has been in Southeast Asia, where people sleep with chickens.

Current cases have proven very mild showing up as pink eye.

“We know that it (the current virus) is a product of Gain of Function because of the research we have done (at his foundation).”

“Research has been done at the USAA Poultry Research Lab at Athens, Georgia and Erasmus University in the Netherlands. The H5N1 virus was found in cattle and sea mammals without a couple hundred miles of Athens, Georgia.”

“Ducks in the world are spreading this, so killing millions of chickens is not going to change this from spreading.”

“There is no government oversight on giving Moderna $176 million to develop a vaccine.”

He also made it clear that we learned from COVID-19 and the Wuhan Lab, that the problem came from scientists using gain of function research, this creating a path for the virus to jump from animals to humans. Let that sink in. In a lab in the US and in the Netherlands, we are seeing gain of function research now on bird flu, a virus that has had little impact on the human population for over 100 years.

“Beginning June 27, 2020, Dr. Nass began a list of deceptive strategies that the Fauci/Pharma/Gates cartel used to control the narrative on hydroxychloroquine and deny Americans access to this effective remedy.” [The Real Anthony Fauci: Bill Gates, Big Pharma, and the Global War on Democracy and Public Health, 2021, Robert F. Kennedy Jr., pg 34]

The following is from her Substack.

Meryl Nass is a physician researcher who was the 1st person to prove an epidemic was due to biological warfare. She revealed the dangers of the anthrax and covid vaccines. Her license was suspended for treating COVID and spreading ‘misinformation.’ [Current numbers of subscribers top 42,000]

The following are just a few points I learned from a post called, The drum beat for bird flu vaccines has begun: nonsensical, couches in a pseudo-scientific jumble of thoughts, July 15, 2024

While there are many “available vaccines”, none of the stockpiled vaccines are matches for the current H5N1.

There is no bird flu virus that transmits from human to human. So how can you tell if a vaccine would work against a future virus.

[Like McCullough] – For this virus to become a problem, it has to gain the ability to transmit from human to human. It also has to become more pathogenic. Outside a lab, the chances of this happening are miniscule.

She then makes this incredible comment, when considering that Finland is already giving farm workers (HUMANS) vaccines for a bird flu virus. “No rapidly produced vaccine has ever been safe and effective. Never. Do you want to be first up to try out the next one?”

I could through “the narrative globalists” versus “the independent medical thinkers” regarding monkeypox, but I want to close this post. I would strongly encourage you to become a subscriber of the excellent substacks of Dr. Peter McCullough and Dr. Meryl Nass. These are doctors at the top of independent thinking who understand there is far more with the vaccine narrative than medical information. They understand because of being censored by the narrative makers for providing “misinformation”, which history is revealing is a Marxist strategy of accusing your opponent of what you are doing. They also look for treatments that have been around a very long time, rather than ones that are “experimental” and have already produced extremely negative side effects in many lives.

In closing, consider the power of one man at the global level of medicine who has no background at all in medicine. How could this much power over any part of global life be good?

“The four organizations had worked together in the past, and three of them shared a common history. The largest and most powerful was the Bill & Melinda Gates Foundation, one of the largest philanthropies in the world. Then there was Gavi, the global vaccine organization that Gates helped to found to inoculate people in low-income nations, and the Wellcome Trust, a British research foundation with a multibillion-dollar endowment that had worked with the Gates Foundation in previous years. Finally, there was the Coalition for Epidemic Preparedness Innovations, or CEPI, the international vaccine research and development group that Gates and Wellcome both helped to create in 2017.”

“So the four organizations that seized control of the global response to COVID had one thing in common, and that was Bill Gates.” [Gates of Hell: Why Bill Gates is the Most Dangerous Man in the World, 2023, Daniel Jupp, pg 296]

After reading the comments of Dr. McCullough and Dr. Nass, we must ask the question, “why the mad dash for a vaccine”?

The U.S. government has awarded $176 million to Moderna to advance development of its bird flu vaccine, the company said on Tuesday, as concerns rise over a multi-state outbreak of H5N1 virus in dairy cows and infections of three dairy workers since March….

U.S. officials previously announced they were moving bulk vaccine from CSL Seqirus that closely matches the current virus into finished shots that could provide 4.8 million doses if needed….

If there ever was a time to seek independent thinkers than global bureaucrats and their partners, it is now.

[If you have not read, WHOse Life is it Anyway?, I encourage you to read it and look at the sources at the end of the post.]

Disclaimer: This information is free. I am merely an American citizen concerned about the continued move away from freedom and toward more controls being pushed at the global level. Like financial information, this information is solely for your own investigation and should not be considered medical advice. Seek independent thinkers. Read. Look for medical emergency solutions established by medical professionals that can help you prepare other than an experimental vaccine praised by globalists as the “only” solution.

As always, comments are always welcomed. If you find this information of value, please share it with others.

If you are reading this blog post, you are like me. You read and seek to understand. You read to grasp changes taking place around you. You read to prepare for your future as well as to have a positive influence on others.

However, as humans, we must also deal with our own desire to not think about things we don’t like thinking about!

If there is one thing I wish I did not have to think about, it is the actions of global organizations that are more and more intrusive into my ability to make my own decisions.

In this post, I am only going to deal with one area and one organization: world global health risks and the World Health Organization.

Random or Pushed

One question I have asked myself often over the years is “random event or an event that was pushed on the public?” On March 11, 2020, we were all hit with the actions of the World Health Organization’s announcement that COVID 19 was now a pandemic.

Just 3 months later, I would watch a recording of a video call by members of the World Economic Forum called The Great Reset. Within a month, Klaus Schwab’s book, The Great Reset was a book anyone could purchase.

The video call confirmed with me that COVID-19 was not the big issue for these non-elected global leaders. In roughly an hour and a half, less than 10 minutes was given about COVIID; the bulk of the time spent on climate change. Why were these individuals not talking about the first global shutdown of the world economy? Why was so little time given to the pandemic?

As I continued to read, I came across Event 201. Immediately I learned that this event took place in October of 2019, months before the world was told we had entered a pandemic by the WHO and the entire world was thrown into an economic shutdown.

The Johns Hopkins Center for Health Security in partnership with the World Economic Forum and the Bill and Melinda Gates Foundation hosted Event 201, a high-level pandemic exercise on October 18, 2019, in New York, NY. The exercise illustrated areas where public/private partnerships will be necessary during the response to a severe pandemic in order to diminish large-scale economic and societal consequences.

As you will notice, this major name in the field of medicine was working in partnership with two of the most powerful organizations in the world, seeking to simulate what would need to be done SHOULD a “severe pandemic” having “large-scale economic and societal consequences” take place in the future.

Now we jump forward to 2022. The following was taken from a webpage called Catastrophic Contagion, a page under the Center for Health Security, the same organization that ran Event 201 in October 2019.

The following can be found on the opening page of Catastrophic Contagion:

The Johns Hopkins Center for Health Security, in partnership with WHO and the Bill & Melinda Gates Foundation, conducted Catastrophic Contagion, a pandemic tabletop exercise at the Grand Challenges Annual Meeting in Brussels, Belgium, on October 23, 2022.

What do you notice? 2 of the 3 organizations that were working on a “fictional scenario” in 2022 were also the same ones that were working on a “fictional scenario” in the fall of 2019 just months before COVID-19 and pandemic became household terms around the entire world.

Once again, let’s review how Event 201 (2019) is described on the Center for Health Security and compare it with how they describe Catastrophic Contagion (2022).

This training tabletop exercise is based on a fictional scenario. The inputs experts used for modeling the potential impacts were fictional. It is a teaching and training resource for public health and government officials.

This training tabletop exercise is based on a fictional scenario. The inputs experts used for modeling the potential impacts were fictional. It is a teaching and training resource for public health and government officials.

If the John Hopkins Center for Health Security and the Bill and Melinda Gates Foundation were partnering with a global organization (WEF) in 2019 to simulate a fictional scenario regarding how public and private entities will be necessary during the response to a severe pandemic in order to diminish large-scale economic and societal consequences… and a few months later an actual scenario, the first global shutdown in history, did take place causing enormous economic and societal consequences… then should we expect another pandemic to “randomly” appear soon since the John Hopkins Center for Health Security and the Bill and Melinda Gates Foundation partnered with another global organization (WHO) in 2022?

Having read and learned a great deal from a host of books, articles, and documentaries since 2020, it is obvious that a lot of people have asked the same question.

If you are reading this post, chances are very high that you have already done a great deal of reading yourself. You have also made decisions about your own health since March 2020 that you may not have made prior to March 2020.

Let me close today with an illustration of WHY this may be hard to discuss with a wide audience even in 2024. I read this in a book that was recommended to me in the summer of 2006. The following is from Professor Jared Diamond’s book, Collapse: How Societies Choose To Fail or Succeed:

“The final speculative reason that I shall mention for irrational failure to try to solve a perceived problem is psychological denial. This is a technical term with a precisely defined meaning in individual psychology…If something that you perceive arouses in you a painful emotion, you may subconsciously suppress or deny your perception in order to avoid the unbearable pain, even though the practical results of ignoring your perception may prove ultimately disastrous.” [Collapse, Diamond, 2005, pg 435]

Diamond then gives an example of how this played out when pollsters interviewed people living downstream from a dam.

“Consider a narrow river valley below a high dam, such that if the dam burst, the resulting flood of water would drown people for a considerable distance downstream. When attitude pollsters ask people downstream of the dam how concerned they are about the dam’s bursting, it’s not surprising that fear of a dam burst is lowest far downstream, and increases among residents increasingly close to the dam. Suprisingly, though, after you get just a few miles below the dam, where fear of the dam’s breaking is found to be the highest, the concern then falls off to zero as you approach closer to the dam! That is, the people living immediately under the dam, the ones most certain to be drowned in a dam burst, profess unconcern. That is because of psychological denial: the only way of preserving one’s sanity while looking up every day at the dam is to deny the possibility that it could burst.” [Ibid, pg 436]

Diamond concludes that even though this is an example of individual denial, this narrative seems to correspond to group psychology as well.

National Sovereignty or Global Tyranny

When I consider how the world was given instructions on daily life by a handful of individuals once the WHO announced that COVID 19 was a pandemic, and how much this event has “reset” the way we look at the world and global groups, I continue to ask everyone to answer the question, “WHOse life is it anyway”? For anyone taking the events of 2020 past their own health to that of how nations came under the power of a global governing agency, it is truly one of the most pressing questions of our time.

As we continue through 2024, I strongly encourage everyone to find sources that focus on developments taking place at the WHO. Clearly, the powers of the WHO are something everyone around the world should be pushing back on, since as shown in 2020, our daily lives can change overnight from such global non elected individuals.

Epoch Times – Excellent interviews, documentaries, and articles

Peter McCullough MD, MHD, – Internist, cardiologist, and epidemiologist: Co-author (with John Leake) of “The Courage to Face COVID-19: Preventing Hospitalization & Death While Battling the Bio-Pharmaceutical Complex.”

Disclaimer: This information is free. I am merely an American citizen concerned about the continued move away from freedom and toward more controls being pushed at the global level. Like financial information, this information is solely for your own investigation and should not be considered medical advice.

As always, comments are always welcomed. If you find this information of value, please share it with others.

In the spring of 2007, I went to Dallas Seminary and met with Dr. Dwight Pentecost. It had taken weeks of talking with my contact at the Dallas Seminary Foundation to arrange this. By this time in my life, I had started my investment research letter, The Investors Mind and had released my research paper, Riders on the Storm: Short Selling in Contrary Winds. Having studied the Bible over 3 decades by that time in my life, I was excited to have an opportunity to talk with a man known as one of the leading scholars in Biblical Eschatology.

Even though he was 92 when we met, our talk was like one with a young man, passionate to tell you of a wonderful trip he had just returned from.

Having traveled the world over, talking with people of many cultures and religions, he told me he had seen a pattern that appeared everywhere he went. There were 3.

They want to have good health. They do not look for “perfect health”, but hope they would not be surprised by something fatal.

They want to have a stable financial situation. They do not want to be rich and fear losing it, or poor, and fear day to day survival. They merely want some stability.

The third one is peace. Peace is not something they could conceive of on a large scale but desire it for their own lives with their family and community.

As I write this post, I dare say a person would need to have turned all communication off with the real world to believe that we live in a world of peace. However, since that discussion in 2007, I have found these 3 concepts to be almost universal as well.

Currently, the world is watching 3 major hotspots: Ukraine and Russia, Israel and Islamic Terror groups, and China and Taiwan. Clearly, the majority of people in the world have no desire to enter a global war. However, I believe we can all see this possibility is high when considering the 3 hotspots above.

What do we know about the History of the Middle East?

If one were to consider the hottest religious hotspot on earth, it would be Jerusalem. This place has centuries and centuries of history for Islam, Christianity, and Judaism. Christianity and Islam (certainly a wide range in what is practiced) are the two largest religions in the world.

If you did not listen to Tucker Carlson’s interview with Putin on X, I would strongly encourage you to do so. When considering the global media narrative that controls “the news”, this one is certainly outside their narrative. It is also contains interesting commentary on the history of Ukraine and its relationship to Russia over centuries.

A great book from a highly seasoned journalist on this topic is Sharyl Attkisson’s, Slanted: How the News Media Taught Us to Love Censorships and Hate Journalism (2020)]. When I talk with individuals, it is not long before I can tell if their ideas have developed from “the narrative”, or if they understand that “the narrative” is akin to indoctrination on the “correct view”. Considering the size of historical events we are watching, understanding the difference has never been more important to how we interpret events.

Do I think there will be peace soon? No way.

Do I think there will be peace in the future for Jerusalem and the area around it? Yes.

Since we are dealing with a world where the global news narrative and censorship continues to get stronger, it is always encouraging to find individuals thinking outside this global narrative box.

If you made it this far, I would like to share with you more information and sources that are outside the global news narrative for your own evaluation of what we are watching in the “Israel-Hamas/Palestinian people” narrative.

The Israeli/Palestinian Conflict Narrative Questioned.

The easiest way to evaluate this statement is to consider what happened BEFORE 1948. I am only going to focus on a few pieces of data.

[2007/my copy was $12.89. Now collectible/over $240 on Amazon.]

We start 50 years ago when she was taken to a refugee camp outside of Beirut.

“ It was 1974, two and a half decades after the war against Israel’s statehood, with several Arab-Israeli wars since, and these appealing, victimized people were still refugees, with weapons as the remedy prescribed for their collective wound. Where were their civil rights? Why were the Arab refugees, unlike refugees on other continents, not yet rehabilitated but still in camps? [italics author’s, page 4]

“Because I’d assumed that Arab refugees from Israel were the ‘Middle East refugees’, I started to find that, also around 1948, whole Jewish populations from numerous Arab countries had been forced to flee as refugees to Israel and elsewhere in the world.” [italics author’s, page 4]

The change of her original hypothesis.

“…this book was nearly two years along and its outline still contained assumptions of conventional wisdom about the pivotal past, unwittingly supporting and reinforcing central misconceptions of the Arab-Israel conflict, even while I was attempting to uncover the truth.” [page 7]

Arab Leaders knew this narrative was wrong decades ago.

“Since 1948 Arab leaders have approached the Palestine problem in an irresponsible manner… They have used the Palestinian people for selfish political purposes. This is ridiculous and, I could say, even criminal” King Hussein of Jordan, 1960 (page 11)

2. Why didn’t the Jews stay in other parts of the Arab world?

After Islam started in the 7th century, things changed. This is only a small sample of the treatment of Jews in Arab nations in the 20th century.

Iraq – “When Iraq joined the Arab war against Israel’s independence, in May 1948, government terror increased; Jews, who had been restricted to some degree from travel, now were forbidden to leave the country, and many fortunes were extorted and confiscated….” “Zionism became a capital crime, and Jews were publicly hanged in the center of Baghdad…the Jews were stripped of million of dollars through economic discrimination.” [page 45]

“The Jews of Iraq, too, flew to Israel – between 1949 and 1952 alone, more than 123,000 Iraqi Jews escaped and were forced to flee to Israel and to leave their assets and communal holdings behind.” [page 43]

Egypt –

“In the days following the November (1947) vote to partition Palestine, Jews in Cairo and Alexandria were threatened with death, their houses were looted, and synagogues were attacked.” [page 48]

“With the outbreak of the 1948 war, Egyptian Jews were barred from leaving Egypt, whether for Israel or elsewhere. Then, early in August 1949, the ban was abruptly lifted, and much sequestered Jewish property was returned.

From August until November of 1949, more than 20,000 of Egypt’s 75,000 Jews fled, many to Israel.” [page 49]

“In 1964 President Gamal Abdel Nasser declared, in an interview, that Egypt still pledged allegiance to the old Nazi cause: ‘Our sympathy was with the Germans.’” [Page 49]

Syria –

“Jewish history in Syria began in biblical times. By A.D. 70, 10,000 Jews dwelt in Damascus, and a consistent Syrian Jewish presence was maintained for more than two millennium….’ [page 60]

“The French were assigned mandatory rights over Syria in 1920, and in 1925, the time of the Druse revolt against the French, the Jewish quarter of Damascus was attacked; many Jews were murdered, dozens were wounded, and homes and shops were looted and set afire. “[page 62]

“In 1942 the Axis radio in Damascus caused additional alarm through broadcast of the false report that Roosevelt and Churchill had promised Syria to the Jews as part of a post-war Jewish state. The Jewish Quarter was raided in 1944 and 1945, and the end of World War II intensified the persecution and restrictions against the Jews. Tens of thousands of Syrian Jews fled between the world wars and after. The Jews numbered roughly 35,000 in 1917; in 1943 about 30,000 remained…By early 1947 only 13,000 Jews remained.” [page 63-64]

At this point it should be obvious from these stories of extreme persecution, that the REFUGEES in this story should be the Jews. The same countries that forced them to flee into the tiny strip of land that became the nation of Israel again in 1948, are offering no aid or help right now to allow the Palestinian Arabs to even take temporary refuge in their own country while Israel fights Hamas and destroys their operations and tunnels still under Rafah. Even Hamas has shown no respect for the Palestinians they are supposed to “govern”.

What does that say to anyone thinking about the global narrative that continues today? This is one of the greatest misinformation narratives of history.

Can there be peace? Yes, but not from the current solutions proposed.

History of Gaza and an Arab Muslim Israeli Speaks Out

I strongly encourage you to listen to these two individuals. With all the painful and negative events surrounding this part of the world today, these two individuals – one Jew, one Muslim, both Israelis – will encourage you that there is a way to move toward peace outside of the two-state solution that neither Hamas, Hezbollah, Iran, or Israel want. I also believe from the writings of various Jews who wrote the Bible I have studied for almost 50 years, that there is a day coming when there will be world peace. The center of that world peace is Jerusalem and this land. I know, just not today.

Next up, good books that have impacted and strengthened my thinking on different topics over the last few months. Their content contains information that is most certainly outside the global media narrative.

As always, comments are always welcomed. If you find this information of value, please share it with others.

It has been almost 3 months since Hamas attacked Israel on October 7th. What started out as an attack by Hamas on civilians – involving the murder, rape, and mutilation of some 1400 civilians in Israel before taking over 200 hostages (women, elderly, and small children) – turned into large protests, calling for freedom of Palestinian people and even for support of Hamas as well as a rise in antisemitism across the world and in universities particularly.

In this blog post, we will ask more questions in our quest to increase our understanding of these recent events.

Q1 – What do we know about the instructions given to terrorists before they attacked? Surely these violent attacks were a smoke screen created by the Israeli Defense?

Israeli security agencies published video footage Monday from the apparent interrogations of seven Hamas terrorists who were captured following the Palestinian terror group’s October 7 onslaught, in which they admitted they had been ordered to carry out atrocities against Israeli civilians.

In one video released by the Israel Defense Forces, a person whose face is blurred said that gunmen were given instructions to kill everyone they saw, including beheading victims and cutting off their legs.

Anyone who followed stories about beheadings by ISIS several years ago knows that violence towards civilians by Hamas is not a new strategy by “modern day” Islamic terrorists. The horrors from videos and articles are so widespread, that for anyone to support HAMAS without questioning their brutal actions is extremely unsettling.

Q2 – What does “from the river to the sea” mean protestors who flooded the streets of London in support of “freeing the Palestinian people” and “their land”?

Following the long held two-state solution created by world leaders over 3 decades ago, Mr. McDonald continues to miss the point that Hamas and most people living in Gaza, “the Palestinians”, do not want “peaceful liberty” or a nation of Israel.

In 1966, the Syrian leader Hafez al-Assad, the father of the country’s current dictator, said: “We shall only accept war and the restoration of the usurped land … to oust you, aggressors, and throw you into the sea for good.” [same Guardian article]

And as the article continued, we can see, whether Hamas or the British home secretary, there are many today who understand this statement, ‘from the river to the sea’ in no way implies a move toward the “two state solution” that world leaders, or globalists, continue to push.

Hamas, whose gunmen killed 1,400 people on 7 October, claim the slogan in their rejection of Israel.

“Hamas rejects any alternative to the full and complete liberation of Palestine, from the river to the sea,” says the organization’s 2017 constitution.

The home secretary, Suella Braverman, tweeted after recent UK protests – in which thousands chanted “from the river to the sea, Palestine will be free” – that the slogan was “widely understood as a demand for the destruction of Israel”. She added: “Attempts to pretend otherwise are disingenuous.” [same Guardian article]

Even the Arabs in Palestine do not accept the two-state solution and were in support of violence by Hamas against Israelis before Oct. 7.

The most recent PSR (Palestinian Center for Policy for Survey Research) poll, published last month (Sept. ’23), showed that if new presidential elections were held today, Hamas leader Ismail Haniyeh would win 58% of the vote, while Mahmoud Abbas would only receive 37%. Hamas’ “armed struggles” (terrorism) against Israel was supported by 58% of the Palestinian public…

Q3 – But surely the Jews should be willing to give up control of Gaza again to the Palestinian people who do not accept a two-state solution?

Unfortunately, the October 7 massacre proved beyond a doubt that both Hamas and the Palestinian Authority actually mean it when they say that they want to annihilate Israel. According to a November 14 poll by the Arab World for Research and Development, 75% of the Palestinians polled support the October 7 massacre and 74.7% support the creation of a single Palestinian state “from the river to the sea”… This is what the Biden administration wants to reward with a Palestinian state? [Does Biden Want Israel to Lose the War?, Gatestone Institute International Policy Council, Dec 22 ‘23]

Amar Tsarfati is an Israeli. He has a You Tube Channel called Behold Israel. He has made videos about the war called Special Middle East Update: The War In Israel. I am linking the one from Nov 1 ’23. Because he is a native-born Israeli, and he has presented much information I have not found elsewhere, I am sharing this with you.

According to Tsarfati, 16 countries have agreed to take in Ukrainian refugees. 0 (zero) Arab countries have agreed to take in any Palestinians refugees. If there were more than 108.4 million refugees (forcibly displaced) around the world at the end of 2022, why does the UN and world leaders focus so much attention on the Arabs living in what was formerly called “Palestine”? Why have other Arab Muslim nations not opened the door to the Palestinian Arabs? If the historical record clearly shows that the Jews were in the land of Palestine before 1948 in large numbers, why is there no mention of the “Palestinian Jews” by the mainstream media when covering this area?

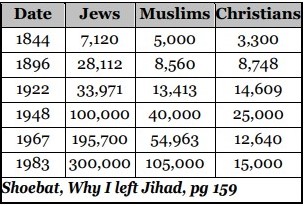

(This grid was prepared for a writing I released in 2009, Jerusalem: City at the Crossroads of History. It can be found at my old, archived website, www.bestmindsinc1.com. Scroll to the bottom. It is a short book with 182 references.)

In my next post, we will investigate history, some modern and some going back centuries, seeking to ask more questions and consider where this story is taking not only the middle east, but the entire world. While this topic is very sobering, I find hope in articles like the one below. Is it possible that two women – an Iranian Jew and an Iranian Persian – could bring us hope and courage? Read on. Back soon. Comments welcomed.

When I was growing up in the 60s and 70s, I watched a detective show called Dragnet. If you are older like me, you may remember Joe Friday, played by actor Jack Webb. As he questioned a new witness in a case he was working on, he would repeatedly say, “The facts, Ma’am”. Just the facts.”

This statement seems quite appropriate as the world continues to watch the Hamas – Israeli War that began on October 7th, and the continued push for a 2-state solution by Arab and World leaders.

In this short piece, I will ask a question like Joe Friday, and provide information for you to consider. Some things are current, and some are centuries if not more than a millennium old. I am uncertain if it will change any opinions, but I would like to share information for everyone to consider.

Q1: What happened on October 7, 2023?

This one is easy. As we can see,across a wide variety of media; Hamas attacked civilians in Israel.

To answer this question I will present 4 points for you to consider; from present to ancient past.

1) It has been widely known for years that Hamas is a terrorist group.

“Hamas’ Record of War Crimes:

Terrorist groups use human shields to cause Western militaries, such as Israel’s, to refrain from lawful attacks or risk being blamed from civilian casualties that are in fact the fault of the terrorist group. This time, Hamas is using not only Gazan civilians as human shields but also the more than 150(highest number is 240) people it has kidnapped from Israel. Hamas has a long history of using human shields as a tactic of war, storing weapons, hiding terrorists, and launching rockets amid densely populated civilian areas, including schools, mosques, and hospitals. ” Hamas Acts to Prevent Northern Gazans from Fleeing South, Foundation for Defense of Democracies, Oct 15, 2023

2) Hamas has proven that they have no respect for human life, no matter what race is involved. This includes civilians who were Chinese, Thai, Russian, French, Turkish, and Arab, as well as Jews.

3) The 1988 Covenant of Islamic Resistance Movement by Hamas reveals that one of the goals of this organization is to kill Jews. The following is found in Article Seven of this covenant.

4) Because the Jews, or more accurately the sons of Israel, did not accept Muhammad’s teachings in the 7th century, he attacked 3 Jewish tribes. One must remember, by the 600s the Tanakh, Old Testament, had been completed for 1,000 years, and the New Testament (all books by Jewish authors other than Luke and Acts) was completed by the end of the 1st century. For this reason, to be faithful to GOD, they would not follow other religions.

The following is an account of the massacre of the men of the Qurayzah tribe in 627 AD. The account is taken from Dr. Mark Gabriel’s work, The Unfinished Battle: Islam and the Jews. Dr. Gabriel was born in Egypt and earned his doctorate degree in Islamic history from Al-Azhar University in Cairo.

“Muhammad and his military put the village under siege for twenty-five days. The Jews were tired and afraid that Muhammad would kill them all. They realized that he would not leave until they surrendered, so they asked to surrender under the same terms as the people of Nadir, who were permitted to leave the village and take along the necessities of life.

However, after the Jews surrendered, Muhammad asked the leader of the pagan converts in Medina what he should do with the Jewish people. This man answered, ‘My judgment is to kill the men and divide the money, women and children among the soldiers.’

Muhammad agreed and told his friends, ‘You judged them with the judgement of Allah.’

Muhammad went to Medina’s marketplace and commanded his people dig trenches. Then they told all the Jewish men to march into these trenches.

As they were going, the Jewish people said to the leader of their tribe, ‘Look at what Muhammad is doing to us. Where do you think they are going to take us, and what do you think they are going to do to us?’

Their leader replied, ‘He is taking us to our deaths.’

Indeed he was. Muhammad and his people killed between eight hundred and nine hundred Jewish men that day. Their form of death was to cut the men’s necks with swords and let them bleed to death quickly. Then they buried the bodies in the trenches. The first part of the advice from Muhammad’s friend had been accomplished. Now the second part.”

After this horrible sight for the woman and children, Muhammad kept 20% of the money, women, and children for himself, giving the rest to his soldiers.

In 628, after he and his men drove the Jewish out of the village of Khaybar, he made a statement that has been practiced right up to the current Gaza War. He declared: “There will never be two religions in Arabia”.

Part 2 and 3

In Part 2 and 3, we will address more questions.

Is there a connection between Hamas and the Al-Shifa Hospital? Has Hamas, since the war they started on October 7th, actually used their own people as human shields? Was the attack on October 7th fostered by a fight for land or was this attack fostered by Muhammad’s words; “There will never be two religions in Arabia”? What has been the history of Jews living in other Arab countries in modern history, or across the Middle East for centuries before WWI?

Every time I post new material on this website, I will alert all readers through my old business website, bestmindsinc.com. You can sign up for free. No promotions, no costs, and infrequent emails.

The last time I posted a blog on living2024 was at the end of 2017. I know, a long gap between posts. However, 2022 is proving to be unlike the last 4 years.

These were the comments from the opening of that 2017 post:

“By 2024, global risks from flagrant financial bubbles in 2017 will have been recognized. For today, one can only seek to influence those willing to think outside the conventional, “‘they’ will take care the big problems” view.

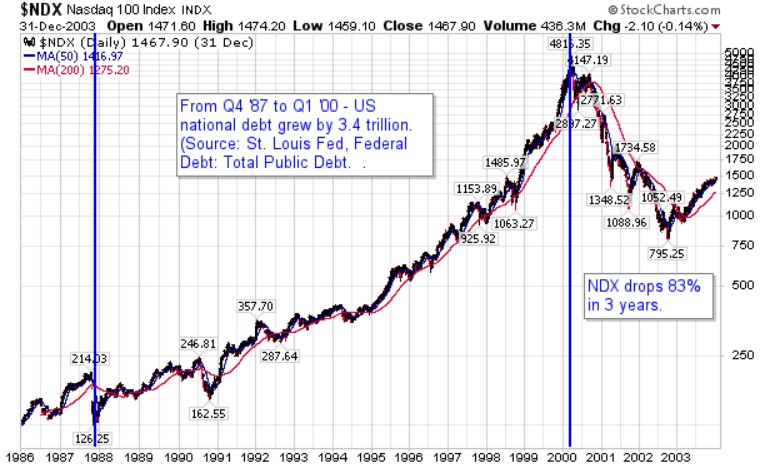

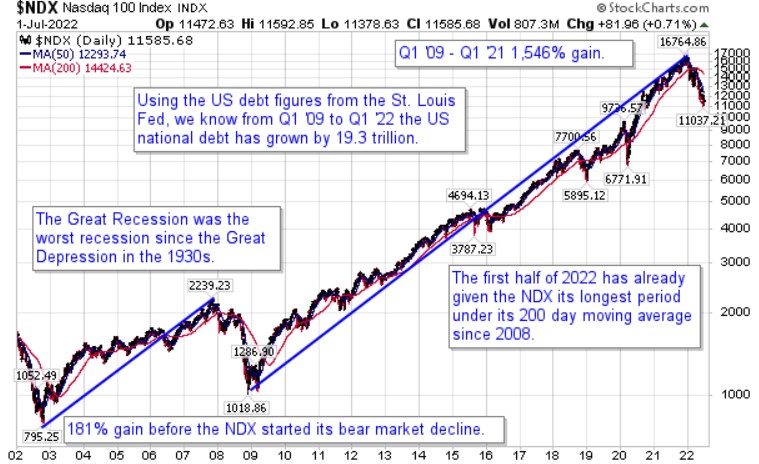

We have just completed the first half of 2022. With consumer confidence hitting its lowest reading since the 1970s in June, it is a good time to review where history has taken us all through the lens of debt growth and stock levels once more. I believe there is a growing understanding that what is taking place across the world is more than just our own stories; it is a major point in history.

There are 3 things not seen since 2009: 1) the longest bull market in the NASDAQ on record, AND 2) the US national debt over 5 times the amount seen in the 1990s, AND 3) a 6-month period where the NASDAQ 100 has traded below its 200-day moving average.

At this point you are either saying, “NOT AGAIN””, or “It always comes back”. But this is not just about the world’s stock markets since most people around the world have no financial interest in stocks. Yet the rise and fall of markets is part of the global economy, and that impacts the lives of almost everyone around the globe.

No matter what your race, nationality, or economic status, for the last half century, the world has been living through the myth of “with more debt and state assistance, we can get back to normal”. Looking at comments coming from those sitting in their globalist chairs, there is no solution that does not include increased control over the lives of billions influenced by their decisions.

If you have read this far, don’t stop. Keep reading!

About 20 years ago, I heard about a book from Dr. James Dobson, founder of Focus on the Family. He stated that outside of the Bible, the best book he ever read was Endurance: Shackleton’s Incredible Voyage. [Short timeline of key dates during the expedition]

When I started the book, I continued to read until I reached the part where they had to depart from the ship because the ice was breaking it apart. With no way of contacting the outside world in 1915 and winter setting in on these men, you knew the story could only get much worse. I stopped reading it. I went to the final chapter. I had to see the end of the story before I could go on.

Reading the final days of triumph over some of the roughest seas on earth in one of the lifeboats, to then climb 32 miles over a steep alpine terrain, revealed that they reached a whaling station at South Georgia Island. Knowing the crew was rescued, I returned to read what was one of the greatest stories of determination and survival.

It is now 2022. We have lived through the growth of the US debt levels by $277 BILLION a year between the ’87 bottom and the ’00 top (12.25 years). We have seen these numbers leap over $7.2 TRILLION ($3600 BILLION per year) between Q1 ’20 and Q1’22. The speed of “money printing” has exploded the US debt in the last 2 years to a level that has been THIRTEEN TIMES that of the 1990s.

How could anyone believe this is the path toward, “sustainability”??!!

No matter what you hear from the world’s largest central banks and global elite forums, the reality is we are all facing historical cycle and historic changes that no bureaucrat can stop. The myth is being crushed, even as it is being promoted even louder.

“Okay Doug, but when do we get to the good part of this story?”

If you need to, jump to my closing remarks and read the extra sources. Then come back and continue reading and thinking. This is not intended to be a quick read.

We press on.

The Present and the Past: Any Connection?

At this point, I want to share with you some of my thoughts about this period from a deeper level. This comes from the last 2 decades of my life and many hours thinking of the period of history I find myself.

Anyone who has been watching the global historical view for the last 25-50 years certainly understands that our world is changing, and some things, not for the better. These changes are also coming faster, as we have seen since the start of 2020.

“Many of us are pondering when things will return to normal. The short response is: never. Nothing will ever return to the ‘broken’ sense of normalcy that prevailed prior to the crisis because the coronavirus pandemic marks a fundamental inflection point in our global trajectory”Covid-19: The Great Reset, Klaus Schwab, 2020

I would agree with Mr. Schwab’s statement. However, I would NOT agree with his solutions.

When studying financial markets, traders and investors look for patterns. As we live in a world of rapid change, is there anything from history past, that help us understand the history unfolding around us?

The following are 3 major trends that have been developing for decades. They seem to relate to the writings of Jewish men from the 1st century AD and prior. Let’s consider them together.

1) Today: At the start of the 20th century there was no United Nations, Federal Reserve, International Monetary Fund, Bank of International Settlements or World Economic Forum. When one considers the planning and actions taken from the UN’s 1992 document, Agenda 21, and more recently, Agenda 30, as well as “The Great Reset” (WEF short video and post in June 2020, and Klaus Schwab’s book (July 2020), it is clear that at the global level of governance, history is not “just one damned thing after another”. [Actually, Arnold J. Toynbee believed there were grand patterns in history.].

Someone is always planning for the future, whether at the individual level or global.

Do you believe we are moving toward a world that protects national sovereignty and the rights of the individual, or a global governing structure that supersedes national sovereignty and human rights decided by small unelected global committees? How could that change our lives?

1st century AD: John, the author of the book of John and Revelations in the New Testament, a disciple of Jesus.

“And the dragon stood on the sand of the seashore. Then I saw a beast coming up out of the sea, having ten horns and seven heads, and on his horns were ten crowns, and on his heads were blasphemous names.” Revelation 13:1

While I have seen maps allegedly developed by the Club of Rome demonstrating how nation states have been grouped into 10 regions, the interesting thing is that the term, “ten horns”, is described 3 times in the book of Daniel (6th century BC), and 4 times in Revelation (1st century AD). From the notes in the John McArthur Study Bible about Revelation 13:1 we find:

“Ten is a number that symbolizes the totality of human military and political power assisting the beast (Antichrist) as he controls the world. Horns always represent power, as in the animal kingdom…”

The Jewish writers of the Old and New Testament produced their writings while living under 6 world empires. I know of no other book that is a collection of writings spanning 1500 years and during 6 world empires. Could this be of value to understanding our world today?

2) Today: If you have every watched the British archaeology show Time Team (1994-2014), you have probably seen a dig where they found Roman coins from the 1st-3rd century. The United States minted its first coin in 1793. We even find Abraham paying 400 shekels of silver for a piece of land to bury his wife Sarah in Genesis 23. This would have taken place around 2,000 years before Christ. Money in the form of a metal coin has a very long history. However, fiat currency is what most of us know as money today.

With the advent of debit cards and apps for smartphones, money has become an electronic swipe. This is the first time in history for societies to ever see this behavior. As such, we are becoming more and more disconnected from the reality of HOW money is formed and what that could mean to our futures.

Away from the smartphone and debit card level, is the top of the global level. The next “tool” to help “stabilize the financial world”…how’s that going…is a digital currency by the world’s most powerful central bankers. What is this? It is an experiment by central bankers. Consider these headlines:

Tie this into the 5 currencies that make up the only international monetary unit, the Special Drawing Rights (launched in 1969). If these banks continue gaining more control through digital currencies and the Special Drawing Rights, they will have even more power over transactions globally.

“A basket of currencies defines the Special Drawing Rights: the US Dollar, Euro, Chinese Yuan, Japanese Yen, and the British Pound.”

Add to these developments ideas discussed in this interview with Catherine Austin Fitts, and this becomes even more disturbing. Fitts has a long history of watching and informing the public regarding changes at the global level of money. Big point: We are moving toward global control of all financial transactions.

1st century AD: John, the author of the book of John and Revelation in the New Testament, a disciple of Jesus.

These are probably the most widely known verses from the book of Revelation. Is it possible these words have anything to do with the current historic trends we see unfolding around us?

“And he causes all, the small and the great, and the rich and the poor, and the free men and the slaves, to be given a mark on their right hand or on their forehead, and he provides that no one will be able to buy or sell, except the one who has the mark, either the name of the beast or the number of his name.” Revelations 13:16-17

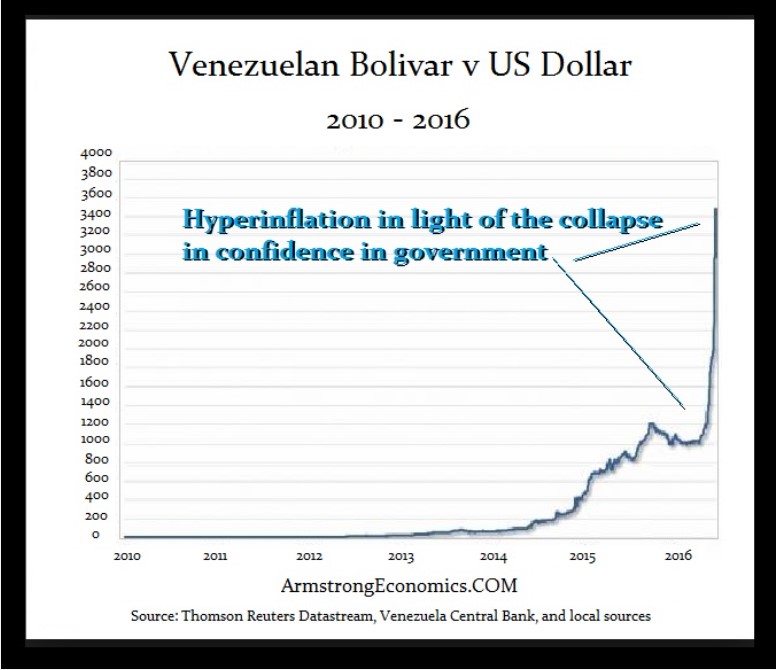

3) Today: If there is one thing felt by almost everyone across the world, it is the reality of inflation and the impact on their lives from the devaluation of their money.

Even one of the most studied economists of the 20th century, John Maynard Keynes, gives us insight into the ROOT of the trouble with monetary instability in his book, The Economic Consequences of Peace (1920):

“Lenin is said to have declared that the best way to destroy the Capitalist System was to debauch the currency. By a continuing process of inflation, governments can confiscate, secretly and unobserved, an important part of wealth of their citizens. By this method they not only confiscate, but they confiscate arbitrarily; and while the process impoverishes many, it actually enriches some…. Lenin was certainly right. There is no subtler, no surer means of overturning the existing basis of society than to debauch the currency…” [Pgs 235-236]

Central bankers, as shown from their actions, have yet to address the problem they are creating by always solving a financial crisis with MORE DEBT (or up next… digital money or CBDC).

“It might thus provoke changes that would have seemed inconceivable before the pandemic struck, such as new forms of helicopter money (already a given), the reconsideration/recalibration of some of our social priorities and an augmented search for the common good as a policy objective…” [Covid 19: The Great Reset, Klaus Schwab & Thierry Mallaret, Introduction, July 2020, highlighted text mine]

1st century AD: John, the author of the book of John and Revelations in the New Testament, a disciple of Jesus.

In the spring of 2007, I met with Dr. Dwight Pentecost, an author and professor who taught at Dallas Seminary for 58 years. He was in his early 90s when we met. We talked for about an hour and a half. It was like talking with a young person, yet with someone who had spoken with people all over the world who was constantly learning.

Since the two books of the Bible most known for their eschatological content are Daniel and Revelation, he told me that he believed that Revelations 6: 5-6 implied a period of hyperinflation.

“When He broke the third seal, I heard the third living creature saying, ‘Come’. I looked, and behold, a black horse; and he who sat on it had a pair of scales in his hand. And I heard something like a voice in the center of the hour living creatures saying, ‘A quart of wheat for a denarius and three quarts of barley for a denarius; and do not damage the oil and the wine.’” Revelation 6:5-6

The John McArthur Study Bible provides commentary that parallels Pentecost’s comments:

“quart of wheat. The approximate amount necessary to sustain one person for one day. denarius. One day’s normal wage. One day’s work will provide enough food for only one person. three quarts of wheat. Usually fed to animals, this grain was low in nutrients and cheaper than wheat. A day’s wage provides enough for only a small family’s daily supply.”

“In Augustus’ time, one denarius was the daily wage of a Roman citizen.”

Closing:

In the first section of this post, I spoke about the book, Endurance: Shackleton’s Incredible Voyage. When the story came to the point where the men had to abandon ship as winter was coming in Antarctica, I had to read the end of the story. Only then, did I return to see how they made it.

To me, the answers to God size problems, is GOD. I know some of you will disagree with me. This is fine and is the basis of free speech and thought. We can have a discussion. We can help each other.

However, it is clear to more and more people that the freedom to have a thought or comment apart from “the information” continues to only be seen as “disinformation”. This is not freedom. This is an Orwellian pathway. This is NOT the right road!

I will continue to write and seek to impact the thinking of others. I will continue to listen to the ideas of others and seek to learn.

To me, it is the only path forward and away from tyranny. To me, the only source powerful enough to deal with a world run by those pushing for more power and control, is a GOD size solution. To me, this is the only way we ever arrive at true lasting peace and respect for all.

The sources listed in the Extra below, are ones I have read many times over decades. I encourage you to read them all if you are unfamiliar with them.

Thank you for taking the time to consider this material.

Extra:Pieces of a GOD size story of hope

Why did Jesus come? John 3:16

Why do we need GOD? Romans 3:23

Is there a price for rejecting GOD? Romans 6:23

Is there a bridge that allows man to connect with the Divine? Romans 10:9-10

Where can one find hope of a GOD size rescue? I Thessalonians 1:9-10, 4:13-18, 5:9-10, I Corinthians 15:51-52

Are there any words about a future time of global peace and rest? Revelation 20:1-3, 21:3-5

Feel free to leave comments about this post, whether pro or con.

By 2024, global risks from flagrant financial bubbles in 2017 will have been recognized. For today, one can only seek to influence those willing to think outside the conventional, “‘they’ will take care the big problems” view.

As 2017 comes to an end, the “perfect” stock market has been drilled into the minds of the American investor like none that has existed in the 121-year history of the Dow Jones Industrials. The chart below, developed by Deutsche Bank, is yet one more example of how 2017 has not only been bullish for stocks but has been at a level of “perfection” not seen before.

Is this a good thing? I think not if one considers the long history of cycles and credit in history. Let me illustrate.

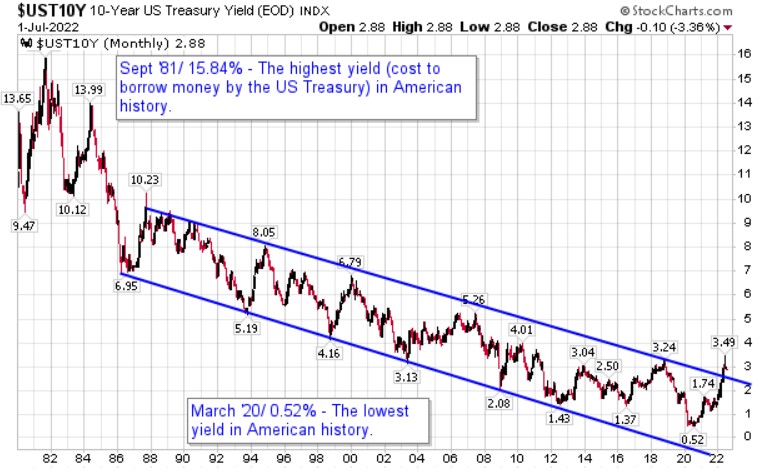

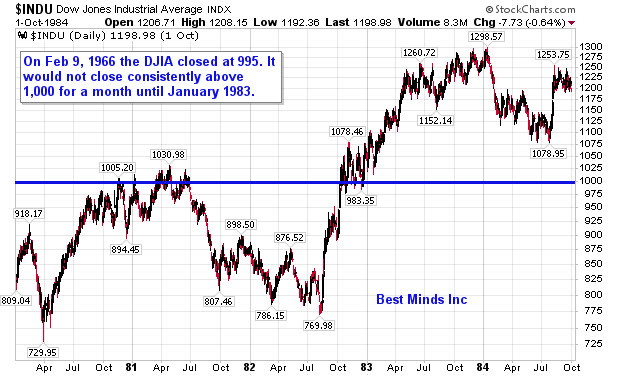

In 1981, I began work on my Master’s degree. Americans would see the national debt top $1 trillion for the first time. If your money market was not paying double digits, you moved your money.

Yields on 10 Year US Treasuries reached 15.84% in October 1981. In January 1983 the Dow closed above 1,000 for an entire month, a first in its history after reaching 995 for the first time in February 1966.

Yes, the money world of the early 1980s differed greatly from 2017.

If someone told us that 36 years later we would see the US national debt climb $1 trillion in a year to cross $20 trillion, money markets at the biggest banks paying less than 0.50% for deposits under 100,000 (a trend since 2014), and the Dow leap 7,000 points over 14 months to almost 25,000…. would we have believed them? Not based on the experience from 1966 to 1981.

So is it hard for us to believe the period ahead might not produce an additional $19 trillion in debt alongside another 24,000 increase in the Dow, WHILE interest rates plunge even LOWER than their LOWEST in American history as seen in 2016?

Cycles have come and gone in history. Bubbles and come and gone in history.

One thing history has taught investors willing to learn from world events since the Dutch Tulip Bulb in the early 1600s is that the more “perfect” any investment theme has captured the minds of the public, the more disastrous the period following when money flowing from the herd changes directions.

The panic to keep from missing out stopped. The panic to get out began.

In the fall of 1981, the cost to borrow money for US government reached its highest in American history.

In the summer of 2016, the cost to borrow money for the US government reached its lowest in American history.

Has this 35-year bond market bull (interest rates coming down, bond prices moving higher) ended?

Could investors learn from the 35-year period leading up to 1981 as we start through 2018?

“The great bear market lasted some thirty-five years, by far the longest duration for a bear bond market in U.S. history. If a constant maturity thirty year 2 ½% bond had been available throughout this second bear market of the century, its price would have declined from 101 in 1946 to 17 in 1981, or 83%. In contrast, in the first bear bond market of the century, 1809 to 1920, the same bond would have declined 35% in price. The recent bear bond market seemed to have much more social and economic significance than that of all earlier bear bond markets. In all the others, bond yields stayed within the traditional band that had prevailed for centuries. This time they broke decisively out of that band.” [A History of Interest Rates, Third Edition Revised (1996), Sidney Homer and Richard Sylla, page 367]

“An entirely new and revolutionary phase of bond market history began in 1965. The Great Society program was underway, and business was assured that never again would even the smallest recession be permitted. Many believed just this. There seemed to be no more risk…..Then suddenly the (bond) market collapsed, led by a sharp decline in the bellwether, the recently issued 4 1/4s of 1987-1992…Market psychology, which had clung to traditional benchmarks was shattered, and the stage was set for a major bear market.” [Ibid, pg 379]

“Greater love has no one than this, than to lay down one’s life for his friends” – Jesus Christ, 1st century AD, John 15:13 [NKJV]

It has been a month now since Hurricane Harvey hit the southern part of Texas, dropping more rain than any storm on record in the U.S. The size and scope are unfathomable when we consider so much change in such a brief time.

Yet in the midst of such devastation, we saw acts of kindness, courage, and sacrifice from average Americans.

Yet another storm has been building for years. The numbers it has produced are staggering. Many have benefited; many have not. However, this storm differs from Harvey and Irma. As this storm has grown, we have been told that we were in recovery, yet like a Hurricane, if we track the storm, we see it has been building in strength, not diminishing.

Let me take one factor in this storm.

Since the $700 billion bailout announced 9 years ago in September 2008 to solve the worst crisis since the Great Depression, we have watched an ongoing deluge of “financial rain” (or debt to buy up financial assets). As I write this in September 2017, the global total of this ongoing “temporary assistance” for financial markets is already over 15 times the original US bailout the world heard in September 2008.

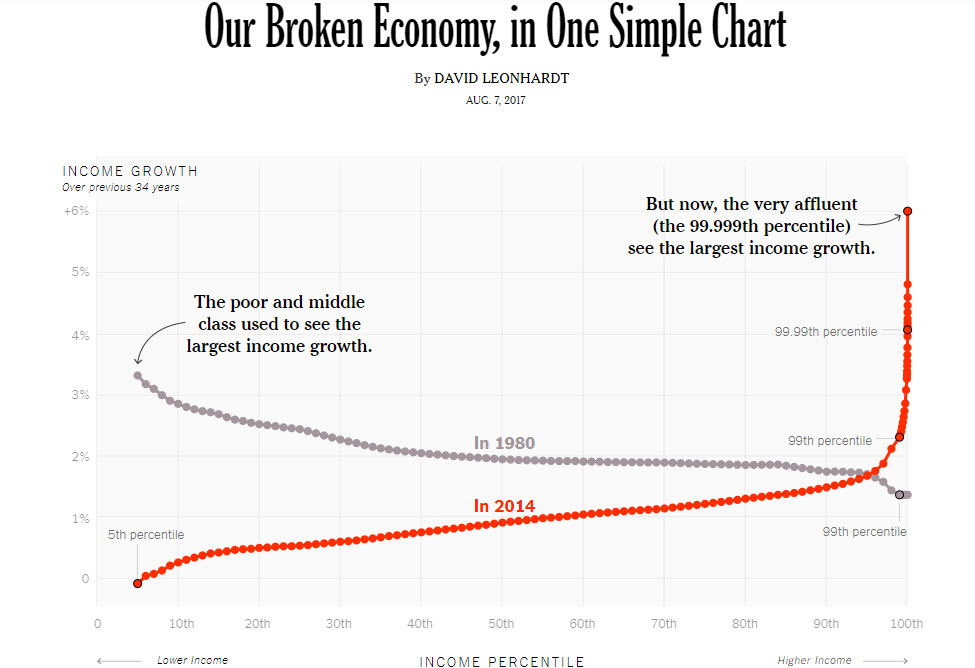

One side effect from the storm that has been building over the last decade, is that it has produced the widest financial inequalities between the top 1% and bottom 90% of any decade in American history.

According to an NY Times article, Our Broken Economy in One Simple Chart (Aug 7 ’17), when I was leaving college in the early 1980s, the middle class and poor were seeing their take home paychecks rise faster than those in the top 1%. By 2014, the torrent of debt to inflate financial assets had flipped income growth on its head; the bottom 90% were declining while only the tiniest of percentages at the top saw their incomes leaping.

In the last decade, the huge gap has not between the upper middle class and the middle class, but between the middle class and the group that make up less than 1/100th of the population.

Has history always shown that the number at the top is small and the number at the bottom is large? Yes. However, never has the wealth of the world depended on so much debt created in this short of a period!

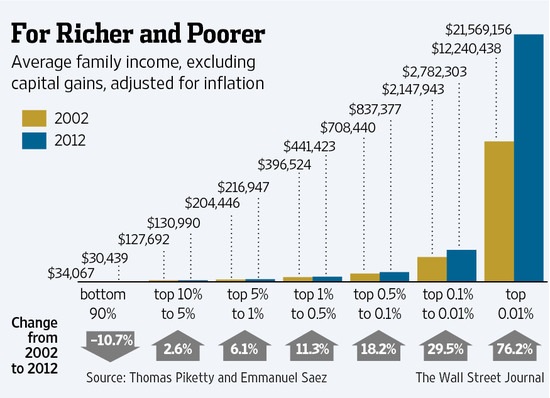

The chart below from the Wall Street Journal is another view of the enormous income disparity that has developed since the “recovery”….and as the chart states, these numbers are now 5 years old, so the widening is even greater in 2017.

So I ask you, have the financial policies followed by the major central banks since 2008 encouraged the idea that all men are created equal?

This short post should not lead one to label the writer as a Democrat or Republican or a Liberal or Conservative, but merely a human being looking at his nation and world and asking questions from the data.

The most powerful force that has elevated the super rich far beyond the rest of the population, whether national or global, has been the Quantitative Easing model followed by central banks. Repeatedly since 2008 we were told this explosion of debt out of thin air, was an attempt to push inflation (prices) higher.

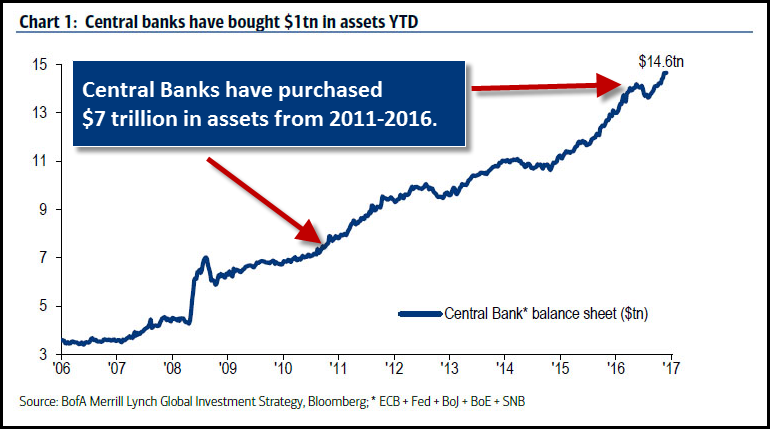

Central banks contributed $7 trillion to BUY ASSETS (chief recipient of the inflation) across the world between 2011 and 2016. YTD an additional $2 trillion has poured into the global financial system to continue this scheme. Keynesian central planning economists call this “the wealth effect”.

But has all this debt, funneled into financial markets producing the second longest bull market in US history, produced rising wages, leading to more spending, or have debt levels increased as wages have declined since 2009?

Yes millions are retired, but with 97 million Americans living paycheck to paycheck, and adults between the working ages of 15 and 64 at 205 million, one can not conclude that overall, the American society is fiscally better off today than when we were lead to believe a $700 billion bailout was enough.

Five years after the S&P 500 bottom in October 2002, the public saw that $8 trillion in stock market wealth had been created. 13 months later, the entire $8 trillion was gone.

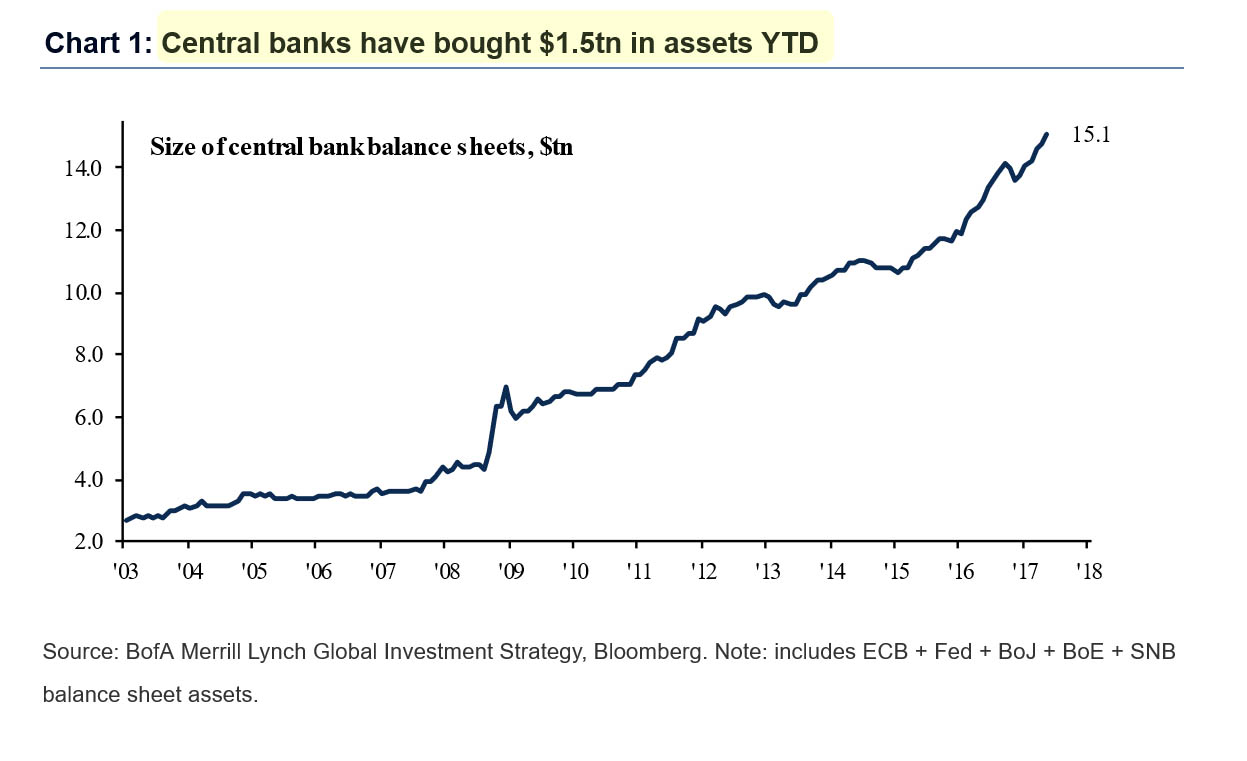

Since March 2009, we have seen US stock wealth climb $19.2 trillion as of September 20, 2017. We can see from the chart below, 5 of the central banks in the world have grown their balance sheets over $11 trillion since the summer of 2008. This had never happened until the 2008 crisis. The debt used to buy these assets and “assist” market prices for 9 years has not gone away.

Are tens of millions of Americans, whether rich, poor, or middle class preparing for the next major financial storm? Will we talk, listen, and work together as this storm sets in, or place our hope in more debt and more “assistance” from our government, who itself sees debt as “unlimited” and the Federal Reserve as the force to calm the financial wind and waves.

“We hold these truths to be self-evident, that all men are created equal, that they are endowed by their Creator with certain unalienable Rights, that among these are Life, Liberty and the pursuit of Happiness.” – The Declaration of Independence, 1776